[ad_1]

As 4th Quarter 2024 earnings season rolls out, we remain bullish on the earnings growth prospects of the retail real estate sector. Each retail REIT is arguably opportunistically priced, but today our focus falls on one company. Slate Grocery REIT (OTC:SRRTF) (SGR.UN:CA) (SGR.U:CA) is cheap by many fundamental metrics, and today its share price just got a new catalyst.

Everybody Should Pile in to Shopping Center Investment

On January 4th, the Wall Street Journal published a compelling article about consumer behavior and how it might translate to real estate investment opportunity. Blackstone (BX) had just agreed to acquire Retail Opportunity Investments Corp. (ROIC) and the article suggested this transaction might be the first of many to come.

Based on retail REIT price performance since, it looks like readers weren’t convinced that shopping centers are an intriguing prospect. SRRTF has managed to hold price better than the peer set, but I would argue that it is cheap and a new, timely buy.

Sector Spotlight: Shopping Center REITs YTD Performance

How Cheap is it?

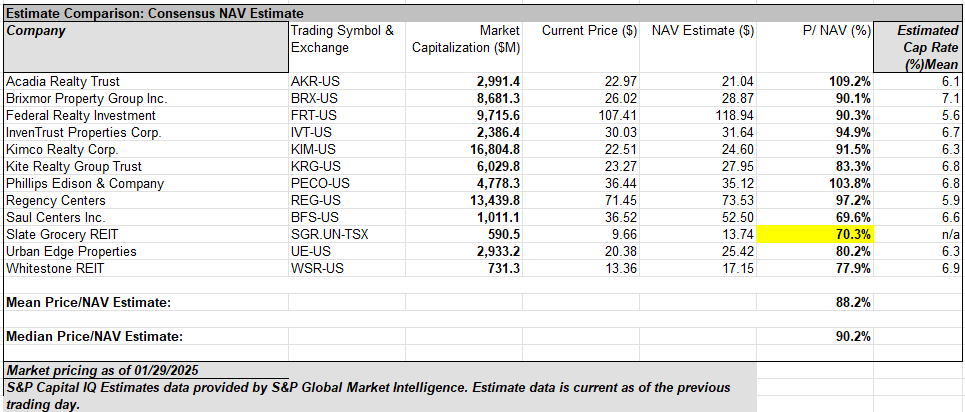

Net Asset Value

According to The State of REITs year-end data, the median equity REIT discount to NAV was 12.92%. In contrast, the shopping center sector median discount to NAV today is just under 10%. At a 30% discount to management’s NAV estimate, it is cheaper than REITs as a whole and very cheap relative to the retail sector.

2MCAC with data compiled from S&P Capital IQ

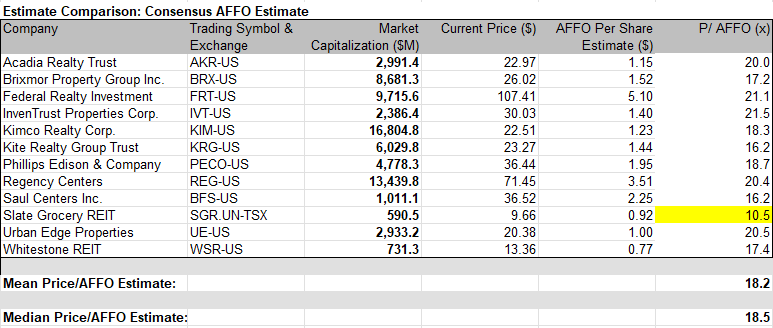

Price to AFFO

As earnings reports roll in over the next six weeks, consensus AFFO estimates will be updated to reflect whatever leasing and NOI progress each company has made in the 4th quarter. By current consensus, the median Price/AFFO for the retail sector stands at 18.5x. In contrast, Slate Grocery, at just 10.5(x), is priced at 57% of the sector multiple.

2MCAC with data compiled from S&P Global IQ

Dividend Yield

As of January 24, 2025, closing prices, the median dividend yield for the whole equity REIT universe was 4.18%. Inclusive of Malls and single tenant retail, like Agree Realty (ADC) and Realty Income Corporation (O), the whole retail sector pays a median dividend yield of 4.13%. In contrast, SSRTF’s $0.072 USD monthly dividend ($0.864 USD/annum) translates to an 8.94% yield as measured against today’s $9.66 share price.

All dividend payouts are not the same, and Slate Grocery for years had a dangerously high payout ratio to AFFO. Steady progress on the leasing front has improved AFFO/share to the point that the dividend appears to be more sustainable. SRRTF’s payout ratio is still much higher than the sector average but is trending in the right direction.

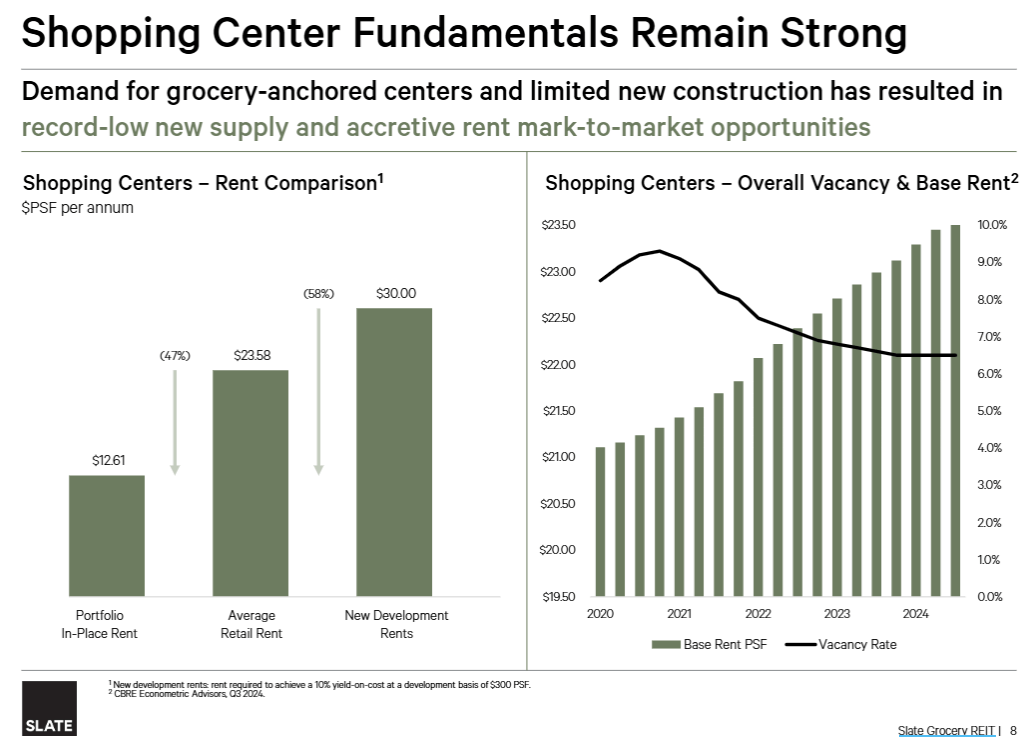

Slate’s portfolio in-place leases are at rates significantly below the average retail rent. With sustaining demand and little new supply, shopping centers are confident that they can maintain high occupancy rates while pushing rents higher. This trend bodes well for dividend sustainability.

SRRTF

The Catalysts

Slate Grocery, like other Canadian REITs, has long carried a higher debt load than the typical US REIT. According to S&P Global data, the retail REIT sector produces a median 4.2x recurring EBITDA/Interest Expense. In contrast, the Canadian REITs produce a median 1.3x recurring EBITDA/Interest Expense, SRRTF currently produces 1.7x recurring EBITDA/Interest Expense.

In the 3Q24 earnings call, Blair Welch confirmed that the company was able to refinance $500MM of debt and that they were in talks to renegotiate terms for an additional $138MM of upcoming debt maturities. Post refinancing, the weighted average 4.8% interest rate provides significant positive leverage and balance sheet stability.

With debt issues addressed, SSRTF management is moving ahead on strategies to improve AFFO growth. On January 29th, they announced the renewal of their share buyback program. Under the normal course issuer bid (the NCIB) beginning on February 3rd, the REIT can repurchase for cancellation up to 5,516,454 class U units, or up to 10% of share float. In reducing the denominator, SSRTF concentrates earnings and per share AFFO and NAV should rise.

If other prior large buybacks are any indicator, the share price could rise as well.

In Summary

We anticipate over the next few weeks that the retail real estate sector will report another strong quarter. We are long about half of the names in the group, but recent developments have emboldened us to get even longer SRRTF.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

[ad_2]

Source link